Market Insight

April 2026

The Rise of Health Intelligence Systems

Capitalizing on the new infrastructure layer of modern care

AI is no longer supplementing healthcare — it is restructuring it. Operators and investors who understand the implicit costs of that shift will define the next decade of health infrastructure.

Veydros Collective

I. The Landscape

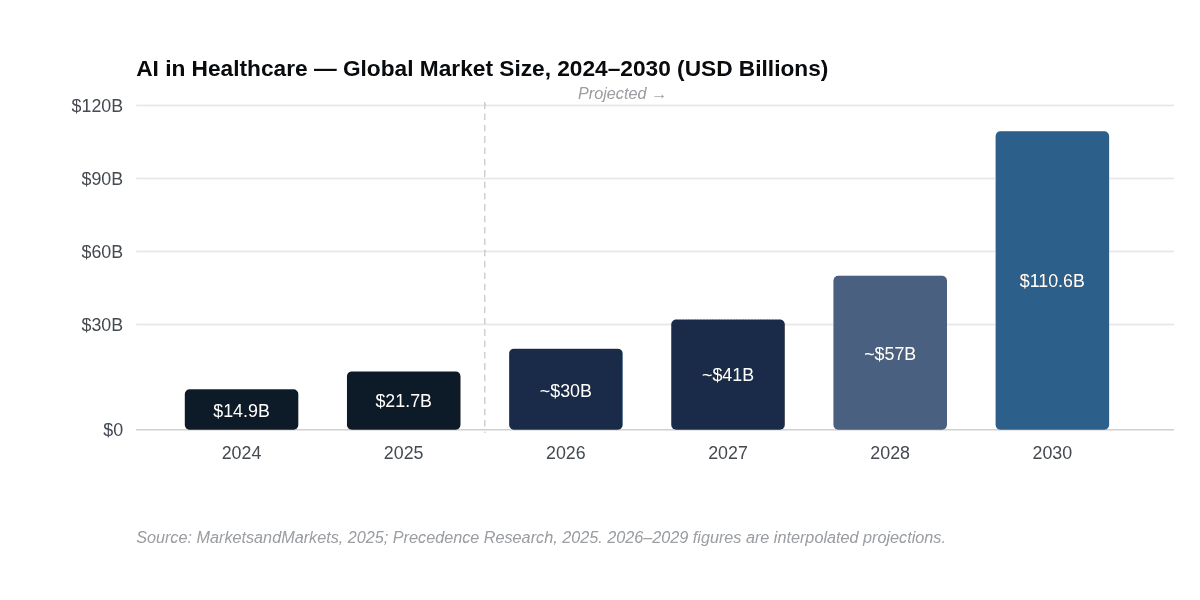

The global AI in healthcare market reached $14.92 billion in 2024 and surpassed $21 billion in 2025. By 2030, it is projected to exceed $110 billion, expanding at a compound annual growth rate of 38.6% — making healthcare AI one of the fastest-growing institutional technology markets in the world.[1] What is less understood is the structural nature of this growth: this is not incremental digitization. It is the emergence of an entirely new market category.

For three decades, "health technology" meant consumer-facing applications — heart rate monitors, fitness trackers, appointment scheduling software. That era is closing. The category now being built is Health Intelligence Systems: AI-native platforms that integrate directly into clinical workflows to interpret data, surface predictions, automate documentation, and support real-time decision-making at the institutional level. The distinction matters because it changes who the buyer is, what the procurement cycle looks like, and what it takes to compete.

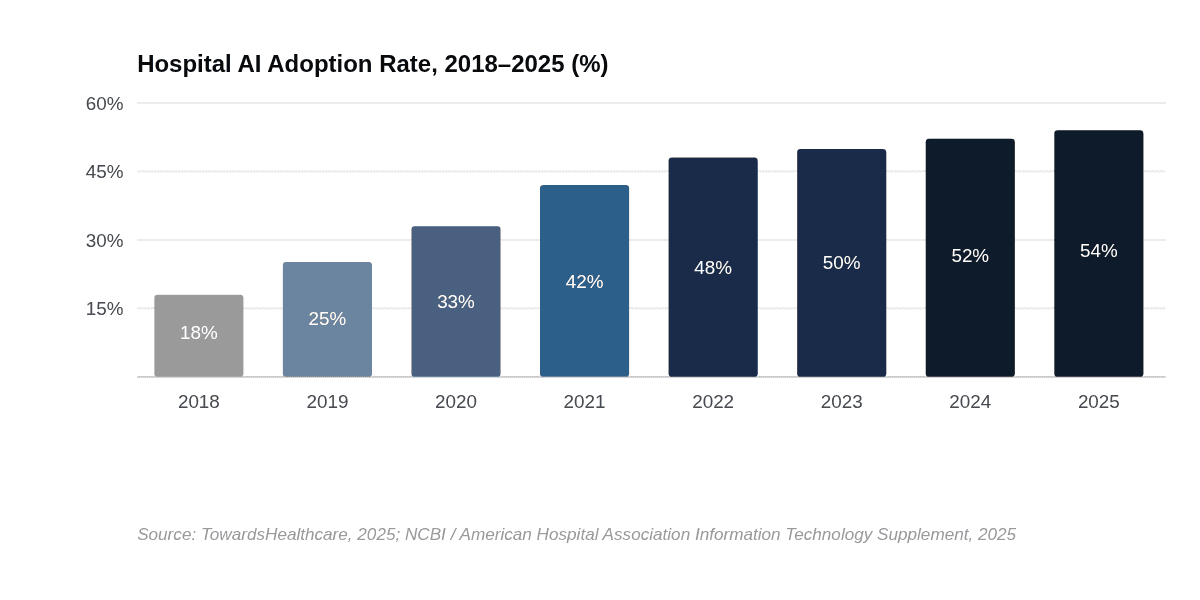

Hospital adoption of AI has risen steadily from 18% in 2018 to 54% by 2025, and 71% of U.S. hospitals now run predictive AI integrated with their electronic health records — up from 66% just one year prior.[2] This is no longer early adoption. For large, system-affiliated hospitals, the figure reaches 86%.[2] The institutional threshold has been crossed. The question is no longer whether Health Intelligence Systems will become core infrastructure — it is who will own that infrastructure layer and at what cost.

Mental health technology sits at the center of this expansion. The global digital mental health market was valued at $27.8 billion in 2024 and is projected to reach $180 billion by 2035 at an 18.5% CAGR.[3] The fastest-growing application segment within digital mental health platforms is workplace mental health and burnout management — a direct consequence of the post-pandemic recognition that mental illness is a workforce productivity problem, not just a clinical one.[4] This has created a new class of buyer: the enterprise health operator, sitting between the traditional provider and the employer, deploying technology across both populations simultaneously.

II. The Dynamics

Three structural forces are producing the current state of the Health Intelligence Systems market. The first is a labor crisis. The U.S. healthcare workforce deficit is projected to reach 18.7 million workers by 2028.[5] AI ambient documentation — tools that transcribe and summarize clinical notes in real time — is being adopted faster than any prior healthcare technology, with leading hospital groups reporting utilization rates as high as 90%.[6] The adoption is not happening because hospitals want to innovate; it is happening because they cannot staff their way out of the documentation burden. Necessity is driving the market more than aspiration.

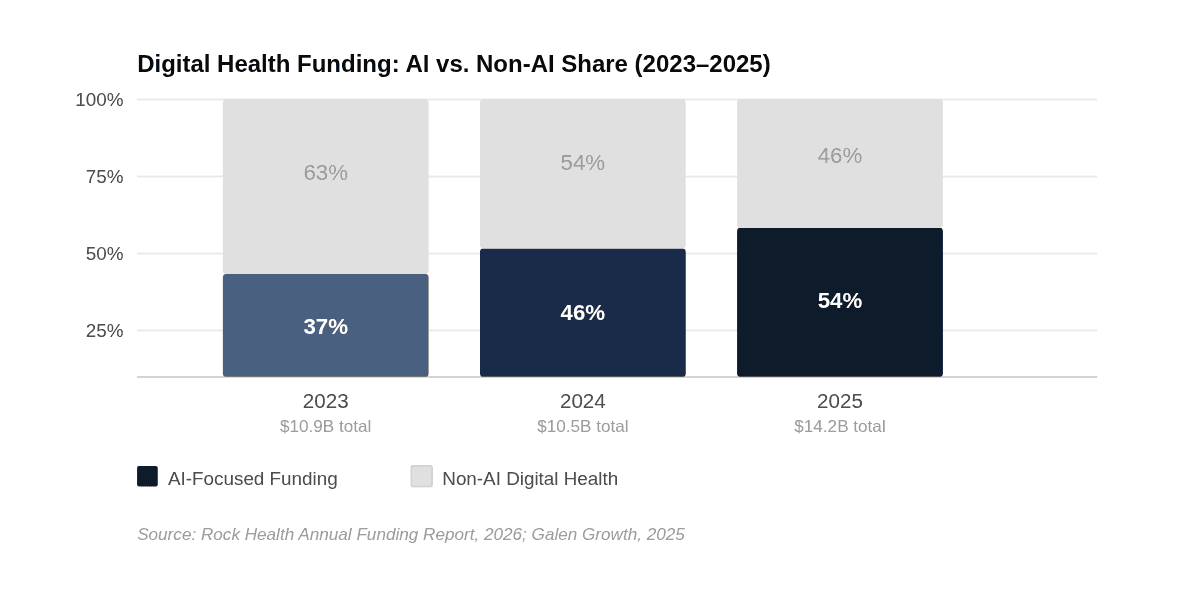

The second force is capital concentration. U.S. digital health startups raised $14.2 billion in 2025 — the highest total since 2022 — with AI-focused companies capturing 54% of all funding, up from 37% in 2024.[7] Merger and acquisition activity nearly doubled, rising to 195 deals from a five-year low of 121 in 2024.[7] The consolidation phase of digital health has begun. Larger, well-funded platforms are acquiring smaller players with specific capabilities — clinical data organization, RCM, care coordination — to assemble end-to-end health intelligence offerings. Companies that cannot demonstrate validated outcomes and scalable revenue are being absorbed or failing quietly.

The third force is the EHR consolidation threat. This is the dynamic most startups are underpricing. Epic Systems currently serves the majority of large U.S. hospitals, and 90% of those hospitals using predictive AI do so through Epic's platform.[2] Epic is now building native AI scribes, virtual assistants, and scheduling agents directly into its product — using the same workflow touchpoints that third-party health intelligence startups depend on for integration. Oracle Health is pursuing the same strategy. The 85% of generative AI healthcare spend flowing to startups today reflects a market window — not a permanent structural advantage.[6]

III. The Shift — The Hidden Cost of Intelligence

The market narrative around Health Intelligence Systems is almost entirely framed around what these systems enable: faster diagnostics, reduced administrative burden, better research throughput, LLM-assisted pattern recognition across patient populations. That framing is accurate, and the market data supports it. But it is incomplete in a way that matters enormously to operators, investors, and the institutions buying these systems.

Health Intelligence is not replacing healthcare workers. It is replacing the margins of error that human redundancy provides. When a physician misses a shift, another physician can cover. When a Health Intelligence System goes offline — or worse, produces a systematically flawed output — the failure propagates across every patient in that system simultaneously. The implicit risk of AI in healthcare is not job displacement; it is a category shift in what a failure event means. The expected cost of a system failure in a hospital environment is not linear — it is exponential. A clinician's absence is a local problem. A HIS outage is an institution-wide event.

The Three Implicit Costs of Health Intelligence Systems

Security & Data Integrity. Patient data held within HIS platforms represents the most sensitive personal information that exists. A breach in a health intelligence system is not a data leak — it is a liability event with clinical, legal, and reputational consequences. As of mid-2025, only ~5% of FDA-cleared AI medical devices had filed adverse-event reports, meaning the actual safety profile of deployed hospital AI is largely unmeasured.[8]

Uptime & Dependency Risk. Hospitals that integrate HIS into core diagnostic and documentation workflows are building operational dependencies on systems with no precedent for reliability standards in clinical settings. A HIS failure at a system-integrated hospital is categorically different from a software outage at a consumer company. The question institutions are not yet asking with rigor is: what is our fallback protocol when the intelligence layer fails?

Patient Welfare & Human Connection. Mental health, in particular, is a domain where the therapeutic relationship — human contact, consistency, empathy — is not ancillary to care. It is the mechanism of care. LLMs can produce clinically appropriate conversation. What Harvard's Division of Digital Psychiatry has documented is that they can also produce convincing but contextually incorrect responses in a domain where psychiatry is "less rule-based" than AI systems are designed to navigate.[9] Deploying AI in mental health settings without robust human oversight structures does not reduce risk — it redistributes it.

None of this is an argument against Health Intelligence Systems. The positive case is well-substantiated: LLMs are reducing clinical documentation time by over 60 minutes per day per clinician, improving adverse event detection in cancer patients by measurable margins, and enabling research environments to surface patterns across datasets that no human team could synthesize at scale.[10] The argument is for a more complete accounting. Operators and investors building in this space must model not just the efficiency gains, but the cost of the system's own failure modes — and design accordingly.

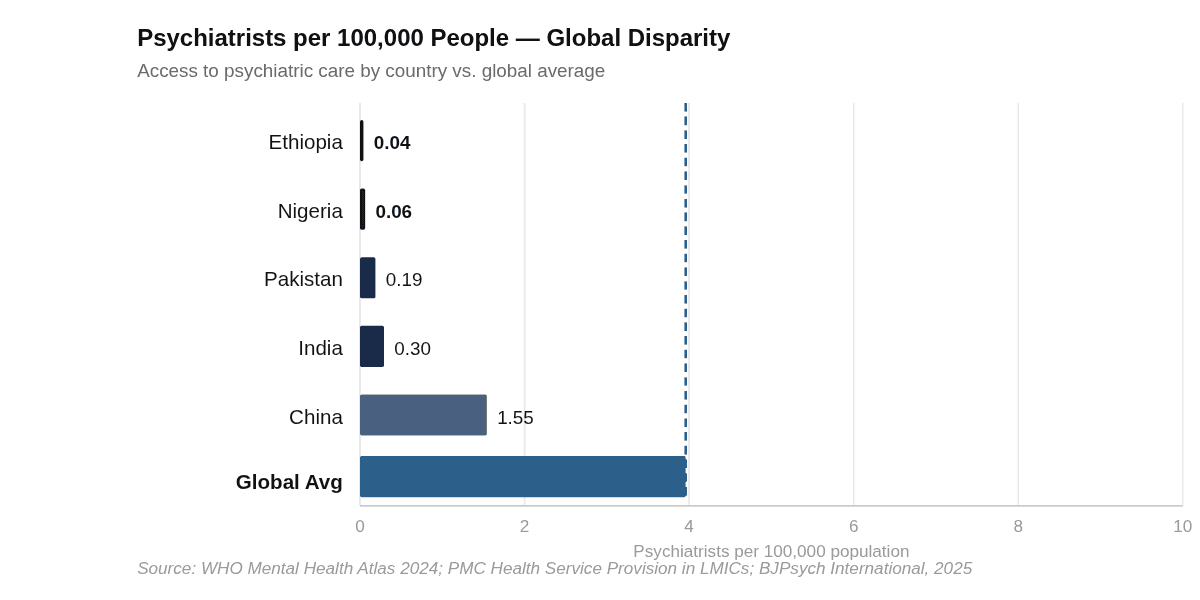

There is also a deeper structural question that the mental health and HIS markets share: what happens to the global population that exists outside the systems these technologies are built to serve? The digital mental health revolution is solving for a population that already has smartphones, internet connectivity, functioning healthcare insurance or employer-sponsored benefits, and basic digital literacy. The WHO's September 2025 Mental Health Atlas — covering 144 countries — found that in low-income nations, fewer than 10% of people with mental health conditions receive any care. In Sub-Saharan Africa, the treatment gap reaches 90%, with some countries reporting fewer than 0.06 psychiatrists per 100,000 people against a global average of 3.96.[11] The technology being built in Toronto, San Francisco, and London is not reaching these populations — and it is not designed to.

This is not merely a social equity footnote. It is the defining structural limit on what "the global mental health technology market" actually means. The $180 billion projection for 2035 is a market that exists almost entirely in countries with per-capita healthcare spending above $1,000 per year. Sub-Saharan Africa's average healthcare expenditure is a fraction of that. The implication for investors and operators is direct: Africa and South Asia represent the largest untreated mental health burden on the planet — and currently, no scalable infrastructure exists to close that gap. This is not an obstacle to the Western HIS market's growth. But it is a fundamental constraint on any claim that HIS is solving the global health intelligence problem.

IV. What to Watch

Five Forward Signals — 2026 and Beyond

CMS TEMPO Pilot Outcomes. The FDA-CMS Technology-Enabled Meaningful Patient Outcomes pilot, launched in late 2025, will generate the first real-world reimbursement data for pre-authorized AI health tools inside Medicare and Medicaid populations. The results — expected in late 2026 — will be the clearest signal of whether digital health tools can graduate from pilot programs to standard payment pathways. This is the unlock that converts HIS from a cost-center story to a revenue-line story.

Epic's Native AI Rollout. Epic has announced AI scribes, scheduling agents, and patient-facing chatbots built directly into its EHR platform. When these features reach production deployment at scale — likely through 2026 — they will define how much commercial space remains for standalone HIS startups inside the hospital setting. Watch the timeline carefully; it is the most consequential competitive event in the sector.

EU AI Act Enforcement Actions. The EU has classified medical AI as high-risk under its AI Act, requiring dual compliance with both the Act and the Medical Device Regulation. The first enforcement actions against health AI platforms — likely 2026–2027 — will define the real compliance cost structure for operating in European healthcare markets, and will set the global standard for jurisdictions following the EU's lead.

Foundation Model Entry. OpenAI, Anthropic, and Google DeepMind are all demonstrating direct interest in healthcare applications. If any foundation model company enters as a health intelligence platform — not just an API provider — the commoditization risk for companies building on top of these models accelerates dramatically. This is the highest-impact tail risk in the sector for the next 24 months.

HIS in Emerging Markets. Africa specifically presents the most significant long-term opportunity in health intelligence that is currently underinvested. WHO's Special Initiative for Mental Health estimates that every $1M spent on community mental health services in LMICs provides access to 2.6 million people at just $0.38 per person.[12] The gap is not primarily a technology problem — it is a financing and infrastructure problem. Watch whether any significant institutional capital (sovereign, multilateral, or private) begins to flow toward mobile-first, low-infrastructure HIS designed for Sub-Saharan Africa. Its absence today is itself data.

V. Strategic Perspective

Strategic Perspective

Looking at this data, two things become clear that are rarely stated together. First, we are watching a new market category permanently integrate into health institutions — not as a layer on top of healthcare, but as its operational backbone. The HIS market is not "health apps." It is a new infrastructure class. That matters for how you evaluate companies in this space, because the competitive dynamics, the procurement cycles, and the failure modes are all categorically different from consumer digital health. The precedent being set right now — which platforms get embedded into hospital EHR systems, which compliance standards get adopted, which vendors get the long-term contracts — will be extremely difficult to dislodge once established. The window to enter at meaningful scale is measured in years, not decades.

Second, the positive case for HIS and mental health technology is real, and it is grounded in some of the most tractable institutional problems that exist: clinician burnout, documentation inefficiency, research data silos, and the inability to deliver mental health support at the scale the workforce demands. LLMs used responsibly in research and clinical documentation are not a speculative bet — they are solving verifiable problems right now. But the framing that dominates this market — efficiency, access, personalization — systematically understates the implicit costs. Patient security is not a compliance checkbox. System uptime in a healthcare context is not a SLA metric. The human element of care — particularly in mental health — cannot be engineered away without creating new and harder-to-measure risks. The best operators in this space are the ones who are building around those constraints, not pretending they don't exist.

On Africa: this is not an emerging market footnote. Sub-Saharan Africa carries a 90% mental health treatment gap and is projected to see a 130% increase in the burden of mental disorders by 2050. The technology does not need to be invented — it needs to be financed and adapted. Mobile-first, community-integrated, low-infrastructure HIS designed for these contexts is not a charity project; it is a generational commercial opportunity that no one is currently positioning to capture at scale. That will change. The question is whether the platforms that capture it are built by people who understand the context, or by Western operators who parachute in with solutions designed for a different world.

MarketsandMarkets — Artificial Intelligence in Healthcare Market Report, 2025 NCBI / American Hospital Association — Hospital Trends in the Use, Evaluation, and Governance of Predictive AI, 2023–2024, September 2025 Market Research Future (MRFR) — Digital Mental Health Market, February 2026 TowardsHealthcare — Digital Mental Health Platforms Market Sizing, November 2025 Future Market Insights — AI in Healthcare Market, citing Becker's Hospital Review workforce projections, 2025 Menlo Ventures — 2025: The State of AI in Healthcare, 2025 Rock Health — Digital Health Annual Funding Report, January 2026 IntuitionLabs — AI Medical Devices: 2025 Status, Regulation & Challenges, October 2025 World Psychiatry / Beth Israel Deaconess Medical Center, Harvard Medical School — The Evolving Field of Digital Mental Health, June 2025 NCBI — 2025 Watch List: Artificial Intelligence in Health Care; Core Solutions Cx360 GO documentation data WHO — Mental Health Atlas 2024; BJPsych International — Mental Health in Africa, 2025; PMC — Mental Health Service Provision in LMICs WHO Special Initiative for Mental Health (SIMH) — cost-effectiveness data, end-2025 report © 2026 Veydros Collective. All rights reserved. This report is produced for informational and strategic purposes. It does not constitute investment advice.

Sources